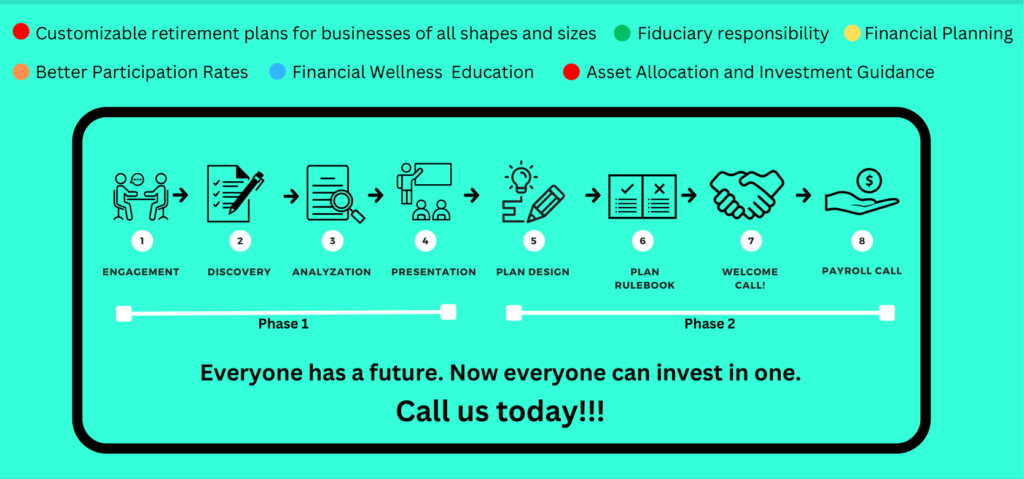

401(k) Advisor Services in Fort Lauderdale

What is a 401(k)?

A 401(k) is a retirement savings plan offered by an employer that allows employees to put a part of their pre-tax salary into the account. Contributions are placed in numerous investment alternatives, such as equities, bonds, and mutual funds, and the funds grow tax-free until withdrawn.

Employers may also contribute contributions to the employee’s 401k account, either through matching contributions or profit-sharing payments. When an employer makes a matching contribution, they match a portion of the employee’s contribution up to a predetermined percentage of their salary. The employer makes a profit-sharing contribution when they put money into the employee’s 401(k) plan.

The IRS has established annual limits on how much an employee may put into their 401(k) account. For employees under the age of 50 in 2023, the contribution cap is $20,000; for those over 50, it is $27,000.

With some exceptions, such as for certain financial circumstances or impairments, withdrawals from a 401k account are subject to taxes and penalties if made before age 59 1/2.

The bottom line is that a 401k is a potent retirement savings tool that can assist employees in saving for retirement while also receiving potential employer contributions and tax advantages. It’s crucial to comprehend the unique guidelines and choices of your employer’s 401k, as well as how they relate to your entire retirement planning. Chris Price Financial Planner offers 401(k) Advisor Services in Fort Lauderdale.

Financial Advisors and your 401(k)

401(k) Advisor Services in Fort Lauderdale

Financial advisors can play a significant role in helping individuals manage their 401(k) retirement plans. The following are some methods financial advisors can help with 401(k) planning:

- Investment selection: Financial advisors can help 401(k) participants select appropriate investment options within their plan depending on their risk tolerance, investment objectives, and time horizon.

- Asset allocation: Financial advisors can assist 401(k) participants establish a diverse investment strategy that is appropriate for their unique circumstances.

- Risk management: By choosing suitable investment options and gradually changing their asset allocation as their risk tolerance changes, financial advisors can assist 401(k) participants in managing risk.

- Retirement income planning: By creating strategies for taking money out of their 401(k) plans and other retirement accounts, financial advisors can assist 401(k) participants with planning their retirement income.

- Tax planning: By creating plans for taking withdrawals in a tax-efficient way, financial advisors can assist 401(k) participants in minimizing taxes on their 401(k) distributions.

- Financial education: To help 401(k) members better understand their plan and how to make wise investment decisions, financial advisors can offer educational materials and other resources.

Not all financial advisors are fiduciaries, which means they are not required by law to operate in their clients’ best interests. This is a crucial distinction to make. It’s crucial to hire a fiduciary financial advisor with experience in retirement planning when choosing one to assist with 401(k) planning.

Converting your 401(k)

Converting a 401(k) account into a Roth IRA is a method that some individuals contemplate in order to potentially lower their future tax liability. Here are some crucial items to consider when converting your 401(k) to a Roth IRA:

- Taxes: You must pay taxes on the amount transferred when converting a 401(k) account to a Roth IRA. Due to the fact that Roth IRA contributions are made with after-tax funds, 401(k) contributions are made with pre-tax funds.

- Timing: Your specific circumstances, including your current tax bracket, retirement timeframe, and other sources of retirement income, will determine the optimal timing to convert your 401(k) to a Roth IRA.

- Not everyone is qualified to make contributions to a Roth IRA. There are income limits for contributing to a Roth IRA, which may effect your ability to make contributions or execute a conversion.

- Benefits of a Roth IRA: A Roth IRA offers tax-free withdrawals during retirement and doesn’t need you to make minimum distributions (RMDs) throughout the course of your lifetime, both of which can be helpful for retirement planning.

- Consult a financial advisor: Converting a 401(k) to a Roth IRA may be a difficult decision with tax repercussions, so it’s crucial to speak with a professional who can guide you through the conversion process and help you decide if this plan is suitable for you.

In conclusion, for some people, converting a 401(k) to a Roth IRA can be a sound retirement planning approach. However, it’s crucial to carefully evaluate any potential tax repercussions and consult a financial advisor to be sure the strategy is in line with your overall retirement objectives.