Income tax diversification defined

Describe how using tax diversification may allow you to potentially increase the amount of after-tax retirement income. Note the different kinds of tax-advantaged accounts and investments available to diversify your tax base. Point out how annuities and life insurance can play a role in tax diversification. |

If you’re saving and investing for retirement, you’re probably familiar with the concept of investment diversification: Combining different types of assets to balance your overall investment risk and return. This same principle can and should be applied to your income taxes.

Why? Tax diversification may allow you to structure withdrawals in retirement to potentially increase the amount of after-tax spendable income.

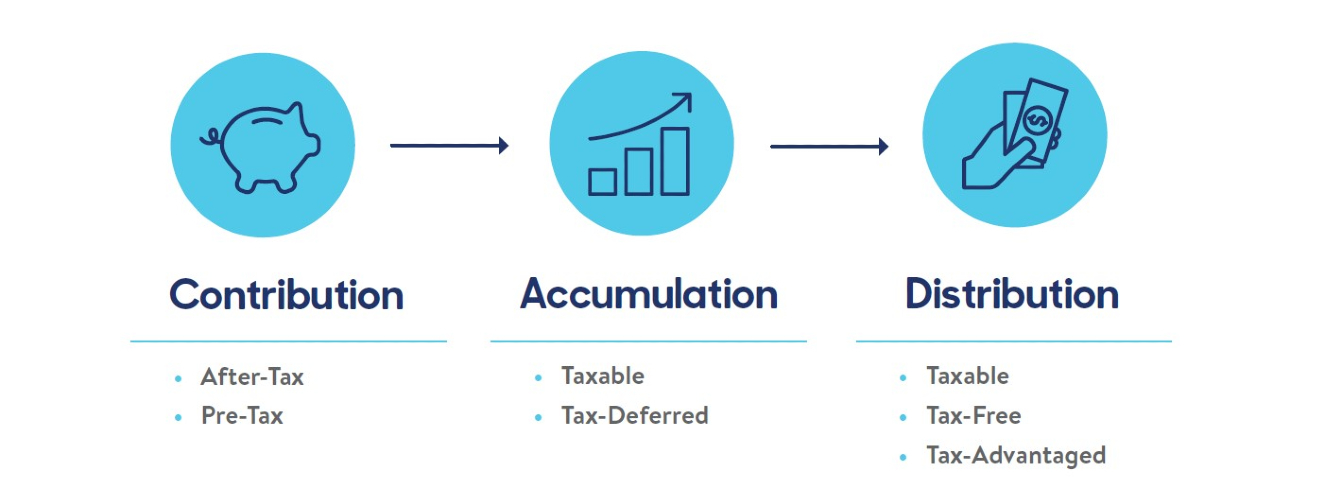

To achieve a diversified tax base, you want financial assets that offer different types of income tax advantages as you:

- Save for retirement (Contribution).

- Grow your savings (Accumulation).

- Use them for retirement income (Distribution).

There are particular income tax advantages offered by different financial instruments at each of these stages.

Choosing options that offer tax advantages during these different stages may help you accumulate more for retirement and reduce your income tax liability during retirement.

To that end, it is important to understand how different kinds of investments and financial vehicles are treated for tax purposes.

After all, regular savings are subject to ordinary income taxes as are direct investments in a personal portfolio, which are generally subject to capital gains taxes as well. But beyond those, there are a range of financial options that are subject to different tax treatment that retirement savers may want to take advantage of.

Retirement savings plans (pretax contributions, tax-deferred accumulation, taxable withdrawals)

As you earn money, you pay income tax. But certain qualified retirement savings programs — 401(k) and 403(b) plans, individual retirement accounts, and some types of pension and profit-sharing plans — allow you to make contributions on a pretax basis. This effectively lowers your gross pay and, as a result, the immediate taxes on that income. (Calculator: How much can I afford to contribute to my retirement plan)

Additionally, many employers and businesses offering these types of plans offer some kind of match of funds to a certain limit. For example, your employer may contribute 50 cents for every dollar you contribute up to 6 percent of your pay. So, hypothetically, if you contribute 6 percent of your pay, then add your employer’s match, your contribution amount is effectively increased to 9 percent. (Related: What is a 401(k)?)

Meanwhile, the pretax income you invested in these types of qualified retirement accounts and plans grows on a tax-deferred basis, meaning the money doesn’t get taxed until you take it out. And then it will be taxed at your ordinary income tax rate.

Since many people expect to be in a lower tax bracket in retirement, these kinds of plans allow some people to keep a portion of their income from being taxed in their maximum earning years, let it grow without being immediately taxed, then start using the income in retirement at a lower tax rate.

These kinds of plans are typically subject to a 10 percent penalty for distributions prior to age 59½, and may also have annual required minimum distributions (RMDs) starting at age 72 (age 70½ for those who reached age 70½ by the end of 2019). Failure to take full RMDs will result in a penalty tax equal to 50 percent of the shortfall. (Related: Understanding RMDs)

In the case of pension and profit-sharing plans, employer contributions and funding are limited. These plans generally offer guaranteed retirement benefits and may allow rollovers to an IRA at retirement. Account value may pass tax deferred to the account beneficiary at death, subject to RMD requirements.

Roth plans (after tax, tax deferred, tax advantaged)

Roth IRAs and Roth 401(k)s are retirement accounts built with after-tax dollars. But both account earnings and withdrawals are income tax free if the owner is 59½ and has had the account for five years or longer. (Related: How a 401(k) combined with a Roth IRA can help younger savers)

Contributions to such accounts, however, are limited. In fact, those making more than a specific income level set by the IRS cannot contribute a Roth IRA. And those who can take advantage of a Roth IRA can only contribute a set amount.

Roth 401(k)s don’t have income thresholds, but do have limits on how much can be contributed each year.

Roth account values may pass tax deferred to the account beneficiary at death, subject to RMD requirements.

Annuities (tax deferred, tax advantaged)

An annuity is a contract with an insurance company that can protect you from the risk of outliving your savings in retirement. It is purchased in a lump sum or series of payments and guarantees a stream of payments at some time in the future. (Related: Types of annuities and how they work)

Annuities are generally purchased with after-tax money. There also exists a certain annuity contract that can be purchased with money from a qualified retirement plan. (Related: Understanding QLACs)

There aren’t any statutory limits on how much after-tax money can be used to fund an annuity, although the annuity itself may have contractual limits.

Earnings in annuities accumulate on a tax-deferred basis. When you start receiving payments from the annuity, you’ll be taxed. If the annuity was bought with pretax funds, the payments will be taxed as ordinary income. If you purchased the annuity with after-tax funds, you would only pay tax on the earnings. (In the case of an income annuity, payments will have an exclusion ratio — a portion of each payment is considered a tax-free return of cost basis.)

There is also a type of annuity — a qualified longevity annuity contract — that can be purchased with money from qualified retirement accounts. It provides a way to delay RMDs and their associated taxes from the portion of the money used to buy this type of annuity. It also helps build a plan for the possibility of living a very long life. (Learn more: Understanding the QLAC)

Life insurance (after tax, tax deferred, tax advantaged)

Life insurance provides a death benefit to help your loved ones carry on in the event of your passing. And life insurance death benefit proceeds are generally income tax free. (Related: 3 tax advantages of life insurance)

But besides protection, some types of life insurance build cash value over time. This cash value grows on a tax-deferred basis.

And the cash value can be accessed on a tax-advantaged basis. Money taken from the cash value of a life insurance policy is not subject to taxes up to the “cost basis.” That’s the amount paid into the policy through out-of-pocket premiums. It doesn’t include any of the tax-deferred investment gains or dividend additions the policy may have had.1 Interest rates on cash value loans from insurance policies may be more favorable than those available for personal loans.

And policyowners can withdraw or borrow against their cash value for any need, like paying a college bill or coming up with a down payment on a house.2 Also, retirees can use the cash value component of a whole life insurance policy as a ready reserve of funds for inevitable market pullbacks, allowing time for invested funds to recover. (Related: How life insurance can help you in your retirement)

Life insurance is typically bought with after-tax dollars. And premiums are limited by coverage amount purchased, which is subject to underwriting limits.

Municipal bonds

Those looking to diversity their tax base also sometimes look at municipal bonds — securities issued by local governments, often to fund infrastructure improvements or special community projects.

The attraction of municipal bonds is that their interest earnings are not subject to federal taxes. They may also avoid state and local taxes if the investor lives in the state or municipality that issued the bond. And there is no limit on how much you can invest.

However, state and local taxes may apply to the interest income if the municipal bonds are held by someone not living in the state or municipality that issued the bond. And capital gains taxes may be due if bonds are sold before their maturity date.

Conclusion

The kind of mix using the various options will be different from individual to individual, depending on age, income, and other circumstances. Many people turn to a financial professional to help them understand the choices and possible outcomes.

The information provided is not written or intended as specific tax or legal advice. MassMutual, its employees and representatives are not authorized to give tax or legal advice. You are encouraged to seek advice from your own tax or legal counsel. Opinions expressed by those interviewed are their own and do not necessarily represent the views of MassMutual.

Provided by Christopher Price, courtesy of Massachusetts Mutual Life Insurance Company (MassMutual). California insurance license number: #4196813.

©2023 Massachusetts Mutual Life Insurance Company, Springfield, MA 01111-0001

MM202609-306811